This article is part of

Accessing Finance in Jordan

As an entrepreneur at the beginning of your journey you will most likely rely on your own savings and ‘bootstrap’ (rely solely on existing resources) through the first few years of your startup. You may also gather funding from what are known as the 3Fs (Friends, Family, and Fools). These are less likely to request guarantees and/or collateral, audited financial statements, or equity in your startup, which you are less likely to be able to provide during the initial phases of your startup. Friends and family, however, are also generally less likely to provide you with the larger amounts of funding you will need at later stages of your growth. You will, therefore, need to access more formal financing entities such as banks, venture capital and private equity funds, microfinance institutions, and others. They offer financing instruments such as loans, equity, mezzanine financing, and grants to help finance your startup’s growth. Understanding these entities, the funding instruments they provide, and their direct and indirect cost is crucial for you to be able to identify the best possible funding avenue for your startup at each stage and accompanying funding round.

The following will provide you with a brief overview of the most prominent financial instruments and modalities available to entrepreneurs in Jordan—grants, debt, equity, and mezzanine financing— and their advantages and disadvantages.

Grants

A grant is a sum of money that is provided by a grantor free of charge to your business (the grantee). A grant is provided in exchange for a startup or entrepreneur’s adherence to certain terms and conditions, or requirements of the grantor, including the continuation or completion of certain activities related to the focus and/or priority of the grantor.

Grants do not require repayment or a share of the business or its profits. They are usually available for non-profit enterprises, however, businesses that have a social impact in areas of interest to the grantor may be eligible to receive grants. Grants can help startups in their early stages as they struggle to obtain other sources of funding, including debt and/or equity investments, due to the small size of their operation, the absence of required financial statements and/or audits, and the limited current profitability of their idea or business. It is mainly for this reason that grants are usually smaller in size in comparison to loans or equity buy-ins, and are generally disbursed in stages according to more stringent milestone requirements, requiring greater and more detailed reporting by grantees.

Grants are usually disbursed by foundations or charities, public or private bodies, including the government or private sector companies (usually as part of their Corporate Social Responsibility), and national and international organizations. They are usually dedicated to specific expenses, such as capital purchases, marketing costs, consultant salaries, etc. A grant can also be provided in the form of an award or as part of a competition. Applicants here will need to show how their business or idea is relevant to the grant. A judging panel then narrows down the field to several finalists from where the winner or winners are chosen.

Grants can also be provided through crowdfunding campaigns (not to be confused with equity crowdfunding), usually done on the internet. Campaigns could be in the form of a donation, as equity funding for a future project or as debt. Crowdfunding could also be provided as payment for a good or product prior to its availability, in order to raise the required amount of funding for its manufacture. Additionally, there is also reward-based crowdfunding, through which funders are provided with rewards following the completion of a project, including, for instance, invitations to a launch party or mentions in the credits of a film they financed.

Grants can either be responsive or strategic/proactive. Responsive grants are those provided by grantors who are open to receiving unsolicited applications from potential grantees, allowing for greater flexibility in the focus of the grantee’s funded activity. Strategic or proactive grants are solicited for a specific purpose, with grant providers publicizing a call for applications and startups having to apply.

Advantages:

- Are given free of charge, with no financial commitments or pay-back requirements

- In some rare cases grantors have commitments to disburse funds and so will approve applications more easily than other funders

- Funders have little influence in the day-to-day operations of the startup

+

Disadvantages:

- Tend to be smaller in size than loans or equity buy-ins

- Have more stringent eligibility, and often extensive, reporting requirements

- Disbursed in stages, usually taking much longer to disburse than other forms of funding

- Providers of grants can be inflexible in accommodating start-ups that need to pivot from one business strategy to another

–

Timeline

|

1

|

|

Grantor receives an application (solicited or unsolicited) from a startup that provides details on its idea and/or goals, operations, financials, and impact. |

|

2

|

|

Grantor evaluates the application. If it determines that a startup has met the eligibility criteria, it assesses the startup in more detail, comparing its performance and potential with other applicants, and proceeds to undertake due diligence. |

|

3

|

|

Due diligence is performed, and a startup’s financial statements, policies, procedures, and operations are audited. |

|

4

|

|

If due diligence confirms the startup and/or entrepreneur to be fundable, and the grantor assesses that all eligibility criteria are satisfied, it disburses funding, either fully or in stages (to ensure adherence to the grant’s terms and requirements). |

Debt

Debt refers to a sum of money given in exchange for payment at a mark-up at a later date. The most conventional type of debt is a loan provided by a financial institution (for example, a bank), at a specified interest rate which the entrepreneur or startup agrees to pay back after a certain period of time.

Banks, microfinance institutions (MFIs) and development banks are the most common source of debt financing, however, debt can also be obtained from family and friends, lending-based crowdfunding platforms, and other financial institutions7. Relevant debt instruments include lines of credit, which are essentially loans that provide cover for day-to-day expenses, as well as factoring or invoice discounting, which involve selling accounts receivables (money owed to a business) at a reduced price.

There are also Islamic, or Shariah-compliant, forms of debt financing. Those are generally tangible, physical, asset-based, and are not interest-based.

The most prominent Islamic financing instruments include

Murabaha

where the seller (usually a bank) buys a good and sells it to a client at a higher final price to be paid in fixed installments.

Mudaraba

where a sum of money provided by the Rabb Al Maal (investor or deposito) is invested by a Mudarib (individual or entity, usually the bank), in exchange for a fee.

Musharaka

where two investors or depositors (including businesses) jointly invest sums of money with profits distributed according to a pre-agreed ratio.

The primary advantage of debt is that it is a cash payment that allows entrepreneurs to avoid giving up equity and can therefore support businesses in expansion if they have stable cash flows and sound projections for growth.

Debt does, however, represent varying degrees of risk and has requirements that not all entrepreneurs and startups can meet or afford. Cash is urgently needed at the early take-off stage of a startup to fuel growth, leaving little room to also take on debt.

Debt providers need to ensure that the borrowing business can meet their obligations to repay the debt. They therefore usually request audited financial statements showing solid cash flows and growth for several years, ruling out most startups at the idea, MVP, or seed stage.

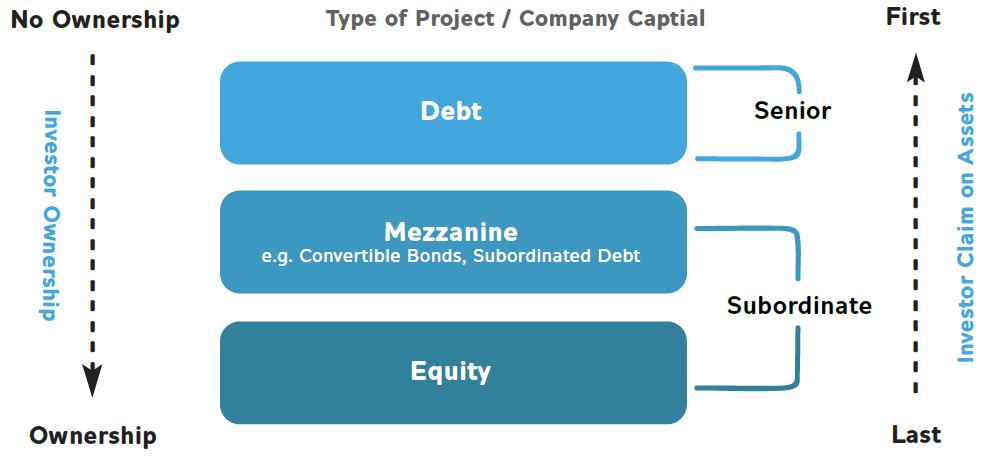

Funders also require proof of collateral and/or guarantees or guarantor/s, in case of default, for what is known as secure debt. Collateral usually takes the form of a physical asset, and is either movable (vehicle, warehouse goods, gold and jewellery, etc.) or immovable (real estate). Secured debt is also usually identified as ‘senior debt’, which is paid first in the event of a company’s bankruptcy and liquidation (sale of assets in an effort to recoup losses). ‘Unsecured debt’, while not requiring the presence of collateral and/or guarantor, charges a higher interest rate to account for the higher risk, and is usually identified as ‘subordinated debt’, which is the last to be paid after liquidation.

Debt can also be expensive to pay back. This is especially the case if projections for repayment are inaccurate or external factors alter the ability of the entrepreneur or startup to repay a loan. This is a risk for the debtor.

Nevertheless, many banks, especially those with a developmental mission, offer ‘soft loans’, which come with easier terms and requirements, including zero or low interest rates, interest ‘holidays’ (a grace period, or a period of time when interest doesn’t have to be paid back), longer amortization rates (period through which debt is reduced through regular repayments), the absence of a need for collateral, and other features that reduce the burden on the borrower.

Advantages:

- Allows the entrepreneur or startup to avoid giving up equity and keep ownership

- Reporting requirements are not as demanding as with grants

- Different types of debt products and services are available to cater to different business requirements

- Defined and predictable payback periods and amounts provide greater room for planning

+

Disadvantages:

- Can be expensive to pay back and presents significant risk for entrepreneurs and startups, especially if financial projections change

- Debtors generally have to present financial statements going back several years, as well as collateral and/or guarantors in case of default, ruling out many early stage startups

–

Timeline

|

1

|

|

Entrepreneur or startup applies for a loan at a bank, microfinance institution (MFI), or other debt provider (e.g. Development Fund). |

|

2

|

|

Debt provider requests supporting documentation, including possibly collateral and/or guarantor, a business plan, and audited financial statements (in some cases a minimum of 3 years). The debt provider may also request a meeting with the entrepreneur or startup for a pitch. If the debt provider wishes to invest in the entrepreneur or startup, they undertake due diligence. |

|

3

|

|

Due diligence is performed, and a startup’s financial statements, policies, procedures, and operations are audited. |

|

4

|

|

If due diligence confirms the startup and/or entrepreneur to be investable, funds are disbursed. |

Equity

Equity financing is the provision of cash in exchange for a share of ownership in a company, and does not represent any repayment commitments on the part of an entrepreneur or startup.

Equity investments are designed to be recouped by investors through the future growth of the company, and as a consequence its revenues, or, through the future sale of part or all of the company (an exit). Equity investments range from a few thousand JOD to millions of JOD, depending on the maturity and size of the startup, from the idea to the series stages, with investments typically made by family and friends, angel investors, venture capital funds, and private equity firms.

Equity investments can present significant risk for the investor, as they are not secured by collateral and/or a guarantor, and companies have no payments to make on any cash owed. Investors therefore minimize their risk through a stringent due diligence process that focuses more on the potential of the team to succeed and the entrepreneur’s idea or startup, as opposed to cash flows and current market share.

The evaluation process for equity investors therefore looks at the potential of a startup or entrepreneur’s idea, the entrepreneur or team’s previous experience and skill set, traction (including in the form of an MVP and expanding and returning user base), and solid business plan and projections. The absence of a guarantee for investors to recoup their investments also means that many investors take more of an active role in the management and operations of a company, depending on the size and share of their investment. It is therefore in an entrepreneur or startup’s interest to seek equity financing from supportive investors knowledgeable in their sector, to better their chances of success.

Laith is an entrepreneur who has recently set up a company. An equity investor values Laith’s company at JOD 10,000 and buys a 10 percent stake in the company for JOD 1,000. Laith’s company grows over time and now has a valuation of JOD 100,000. The investor’s original stake of 10 percent increases from JOD 1,000 to JOD 10,000, multiplying his equity investment by 10.

Advantages:

- No commitments to make cash repayments

- Supportive and knowledgeable investors can make the difference for the success of a startup or entrepreneur

+

Disadvantages:

- Giving away too much equity too early can severely limit the ability to fundraise at later stages, thereby holding back growth.

- Giving away equity and ownership will lessen control of entrepreneurs and decrease their financial returns

- Impatient investors looking for quick exits can cripple startups

–

Timeline

|

1

|

|

Entrepreneur or startup approaches investor for funding. |

|

2

|

|

If interested, investor invites entrepreneur or startup to a meeting to learn more or go through a pitch, understand the entrepreneur or startup’s exact request (amount of funding in exchange for percentage of equity), and may request additional information, including financials, business plan, and references as part of due diligence. |

|

3

|

|

Due diligence is performed, and a startup’s financial statements, policies, procedures, and operations are audited. |

|

4

|

|

If due diligence confirms the startup and/or entrepreneur to be investable, investor disburses funding and monitors performance of startup and adherence to terms and conditions of funding. |

Mezzanine

Mezzanine financing is a hybrid of debt and equity, and provides the lender the right to convert their loan, sometimes at a cheaper rate, into an equity stake in a company at the closing of a new round of funding or in case of default. Mezzanine is subordinate to senior debt and senior to equity—this means that mezzanine providers, in case of a company’s default, receive their money after regular debt providers and before equity owners.

Mezzanine financing is the most complex of the aforementioned funding modalities, mainly because it combines different forms of funding at different stages and is highly customizable. It can therefore offer greater flexibility to lenders and borrowers.

Borrowers generally only access mezzanine financing when they need access to cash quickly. And as mezzanine financing is unsecured, its interest rates are higher than regular debt. Additionally, borrowers may need to make interest payments more frequently than for regular loans, including every month or quarter.

The most prominent type of mezzanine financing is a convertible note: debt that can be converted to equity. This is helpful for companies that still cannot determine their value, especially if they are at an early stage of their growth or operation. While convertible notes specify dates when a company needs to repay the debt (maturity dates) and interest rates, such debt can be converted to equity in the company, according to preset valuations and rates

If an investor and a startup agree on a JOD 100,000 convertible note with a 40% discount, this means that when the startup raises money at a future round, the investor will be able to purchase shares of the company at 60% of the price other buyers would be forced to pay. So, if a startup’s shares are priced at JOD 10 during a funding round, the mezzanine investor would be able to buy each share at JOD 6.

Advantages:

- Can offer greater flexibility and reduced risk for lenders and borrowers—lenders can have the best of both worlds (debt and equity), while borrowers can have quicker access to cash

- Can offer better funding terms for entrepreneurs than simple equity since it mitigates risks for investors

- Can delay the valuation of a startup at an early stage, enabling it to reach a more accurate valuation at later stages

+

Disadvantages:

- Can be expensive and very complicated to structure correctly, especially for inexperienced entrepreneurs

- Entrepreneurs may need to make regular payments to funders

–

Timeline

|

1

|

|

Entrepreneur or startup approaches investor for funding. |

|

2

|

|

If interested, investor invites entrepreneur or startup to a meeting to learn more or go through a pitch, understand the entrepreneur or startup’s exact request (amount of funding and modality—equity or interest payment, or a combination of the two) and may request additional information, including financials, business plan, and references as part of due diligence. |

|

3

|

|

Due diligence is performed, and a startup’s financial statements, policies, procedures, and operations are audited. |

|

4

|

|

If due diligence confirms the startup and/or entrepreneur to be investable, investor disburses funding and monitors performance of startup and adherence to the terms and conditions of funding. |

Impact Investing

Impact investing is defined as investing that is “made with the intention to generate positive, measurable social and environmental impact alongside a financial return.” Impact investors can be individuals and/or institutions, including banks, investment funds, governments, and others.

Characteristics that define impact investing include:

Intentionality: investments that are made with the intention to generate positive social and/or environmental returns.

Financial returns: impact investments are made with the expectation that they will also generate financial returns. These returns may be below, above, or equal to the market rate.

Range of asset classes and funding modalities: impact investments can be in the form of debt and/or equity.

Impact measurement: since impact investors invest to generate impact, they tend to employ robust measurement metrics to ensure their investments are truly making an impact.

Advantages:

- Many businesses are not ready to be able to measure their growth or targets according to occasionally more costly and more detailed standards and/or metrics (including social and/or environmental indicators) impact investors can require

+

Disadvantages:

- Can be expensive and very complicated to structure correctly, especially for inexperienced entrepreneurs

- Entrepreneurs may need to make regular payments to funders

–

The table below provides a comparison of the most salient aspects of the various financing instruments.

| Financial Instrument |

| Aspect |

Grant |

Debt |

Equity |

Mezzanine |

| Funder |

Donors

National and International Foundations

Private Corporations (CSR)

Crowdfunding Platforms |

Banks

Microfinance Institutions (MFIs)

Private Lending

Development Funds |

Angel Investors

Venture Capital Firms

Private Equity Funds

Crowdfunding Platforms |

Investment Funds |

| Acquisition of ownership |

No |

No |

Yes |

Sometimes |

| Cost of Financing |

Negligible |

Medium to High |

Medium |

Low to High |

| Financial Risk to Funder |

Low |

Low (due to collateral and/or guarantor) |

High |

Low to High |

| Financial Return to Funder |

None |

Interest payments |

Dividends with continued ownership, or cash in case of an exit |

Interest payments, and/or cash or dividends, depending on structure of financing |

| Provision of Support to the Entrepreneur |

Low to High |

Negligible |

Medium to High |

Low to Medium |

| Use of fund s |

Mostly restricted |

Somewhat restricted |

Mostly unrestricted |

Mostly unrestricted |